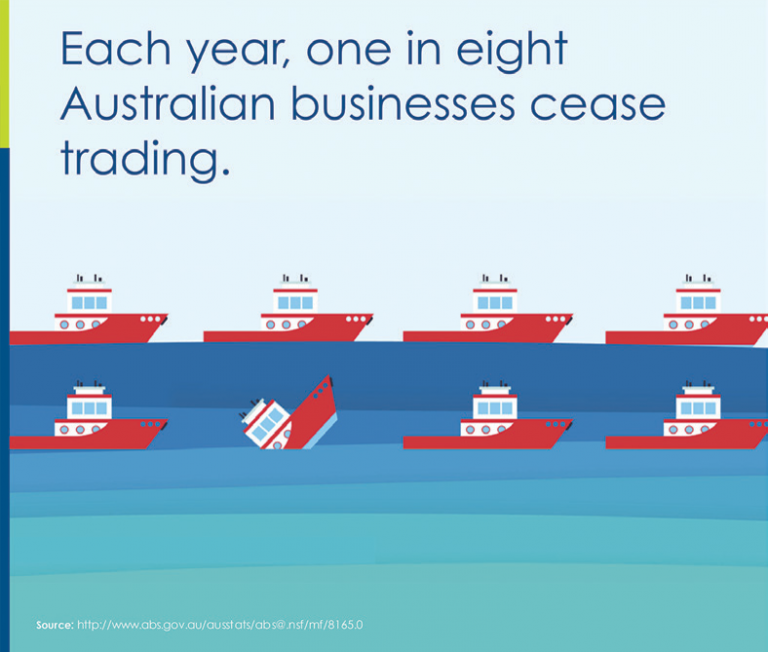

Build a cash reserve

Cash is king and poor cash flow can result in being rejected from loans you need to grow your business or cover yourself during downturns in business activity.

To maintain a consistent cash flow it’s important to build a robust cash reserve which can help you meet your financial obligations in difficult times and allow you to take up opportunities when they present themselves.

To build your cash reserve take care that you are paying your invoices on time and getting paid on time by your customers. If you have any bad business debts, take a look at how you can reduce them. An outstanding tax bill can be a huge hindrance to cash flow so talk to a professional about getting this under control.

Separate business and personal money

By keeping business and personal expenses separate, you may better understand your business’s cash position.

It may also ensure that you don’t use money meant for your business on personal expenses and conversely can help make sure you are paying yourself a wage from your business.

Control business costs Controlling costs might help you to maintain healthy cash flow. This may mean taking a hard look at the practices and processes you have in place and determining if they are efficient or eating up too much of your time.

Identify where you are wasting time and money and consider if you can make changes without sacrificing growth or diminishing the client experience.

Take a good look at stock levels, supplier terms and rates, customer engagement, loyalty and ease of transaction.

Predict your growth

Having a view of expected business growth can help you to map out when there may be ebbs and flows so you can tighten up spending when income is low. The 2019 survey reported that revenue sentiment in SMEs was growing, and metropolitan businesses were more positive than those that were regional based. The figure of expected growth in metro areas was 58% compared to 47% in regional areas2.

Protect your business

Taking out business expenses insurance and key person insurance may help meet business running costs if a key employee is too ill to work. Both insurance plans provide a monthly benefit if you or a key person in your business become incapacitated which protects you, your business partners, family and, the reputation of the business which is paramount to your ongoing success, particularly if the time comes that you need to sell up.

Do you have a trusted adviser?

Each small business is different and the way the owner wants to run their business is different so it’s wise to seek advice tailored to your business. Whilst the opinion of family, friends and colleagues is important, professional advice is paramount.

Scottish Pacific and East & Partners, October 2018, ‘SMEs flag higher revenue growth, but prospects could be dampened by declining property market and cash flow issues,’ accessible at: https://www. scottishpacific.com/media-releases/smes- flag-higher-revenue-growth-but-prospects-could-be-dampened-by-declining-property- market-and-cash-flow-issues

2. SME Growth Index September 2019 https:// scottishpacific.com/images/General/ SPC11500-SME-Growth-Index_AW2_Digital. pdf

IMPORTANT NOTE: The information provided in this document, including any tax information, is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial situation or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser.

The views expressed in this publication are solely those of the author; they are not reflective or indicative of Financial Services Partners’ position and are not to be attributed to Financial Services Partners. They cannot be reproduced in any form without the express written consent of the author.

From time to time we may send you informative updates and details of the range of services we can provide. If you no longer want to receive this information please contact our office to opt out. This information is correct as at February 2020.

Financial Services Partners Pty Ltd ABN 15 089 512 587, AFSL 237590