Forecasting the general level of house prices is difficult at the best of times. Many factors can influence prices including how high or low interest rates are, vacancy rates, location and so on. Heading into the current period, we saw strong house price growth into late March supported by cuts to interest rates.

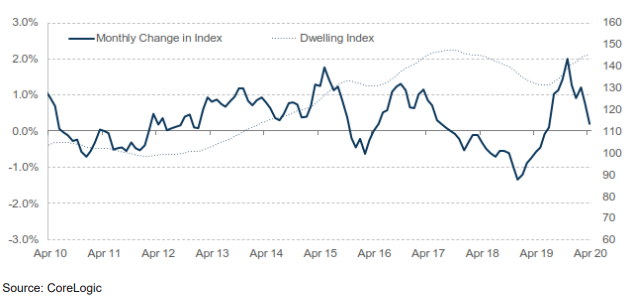

Monthly change in Home Value Index (5 capital city aggregate)

However, as the full impact of the current crisis plays out, we believe that there is an increased likelihood that

house prices will fall. The extent of these falls will depend on the length of time of both the health and economic

slump we are experiencing persist.

Our rationale includes:

• Unemployment remaining at high levels with weak income growth means less ability for people to obtain

and afford mortgages.

• Emergency government payments such as Jobkeeper are only meant to last until September 2020

resulting in weaker incomes and less money to afford existing or new mortgages.

• Bank lending is likely to be challenged given banks are more reluctant to lend in a weaker economic

environment. This would suggest less money chasing property and an overall negative for prices.

• Mortgage rates are at their all-time low and unable to fall much (if any) lower. This is a sharp contrast to

previous recoveries, which experienced tailwinds from falling mortgage rates that had boosted potential

buyer borrowing power;

• International migration, including overseas students, has been an important source of housing demand,

especially in Sydney and Melbourne. Lower demand for housing will see rising vacancies and pressure on

prices.

• Rising housing supply with a large pipeline of apartments being completed and short-term rentals like

Airbnb returning to the long-term leasing market.

• Rents are likely to fall on the back of rising supply and increased unemployment.

Critical to how low property prices fall (or “correct”) is how well Australia contains the coronavirus and reopens

the economy. At the time of writing, we have done very well, especially compared to most of the rest of the

world. This should see us begin our economic recovery sooner, helping to reduce the downward pressure on

prices.

How could this impact you?

While all housing may be affected to some extent by the factors we have outlined, your specific circumstances

may be different. For example:

• Some regions are more reliant on how a specific industry is doing as opposed to the broader market.

• Capital cities outside of Sydney and Melbourne have, on average, delivered less capital growth. Most returns have come from the rent generated and will likely continue barring a new substantial pick-up in demand e.g. Perth in the mining boom.

However, there is an overriding danger given the scale of the economic slowdown. In the recession during the early 90s, Australian property held up reasonably well with the ABS House price index seeing a maximum loss of ~3% on average for Sydney. However, we have also had slumps outside of a recession such as the 2017-2019 period.

To give perspective on the impact the current experience could have, the major banks have issued their own

baseline forecasts, such as;

• Westpac has forecast an overall decline of -15% in 2020 and -5% in 2021.

• Commonwealth Bank has forecast an overall decline of -11% over 2020-2023.

These forecasts estimate the range of outcomes that could occur over the next couple of years. We also note that these forecasts do not necessarily allow for positive factors such as government intervention. For example, if State Governments removed stamp duty (one reform being discussed) this could help offset some of the weakness we are anticipating by removing a substantial transaction cost currently in place.

As with any investment, property investors should continue to monitor conditions and ensure it continues to meet their objectives and goals together with professional advice. It is important to remember that property will, most likely, not be your only asset. Through superannuation you will be diversified into other investments that are unlikely to experience the same results.

Speak to us today if you would like to discuss your overall positioning and how you are tracking towards your long-term goals.

The information provided is general in nature. It has been prepared without taking into account any of your individual objectives, financial situation or needs. Before acting on this advice you should consider the appropriateness of the advice, having regard to your own objectives, financial situation and needs. This publication is prepared by IOOF for: Bridges Financial Services Pty Limited ABN 60 003 474 977 AFSL 240837, Consultum Financial Advisers Pty Ltd ABN 65 006 373 995 AFSL 230323, Elders Financial Planning ABN 48 007 997 186 AFSL 224645, Financial Services Partners ABN 15 089 512 587 AFSL 237 590, Millennium3 Financial Services Pty Ltd ABN 61094 529 987 AFSL 244252, RI Advice Group Pty Ltd ABN 23 001 774 125 AFSL 238429, Shadforth Financial Group Ltd ABN 27 127 508 472 AFSL 318613 (‘Advice Licensees’). This publication is not available for distribution outside Australia and may not be passed on toany third person without the prior written consent of the Advice Licensees. The views expressed in this publication are solely those of theauthor; they are not reflective or indicative of the Advice Licensees position and are not to be attributed to the Advice Licensees. They cannot be reproduced in any form without the express written consent of the author.