What’s changing?

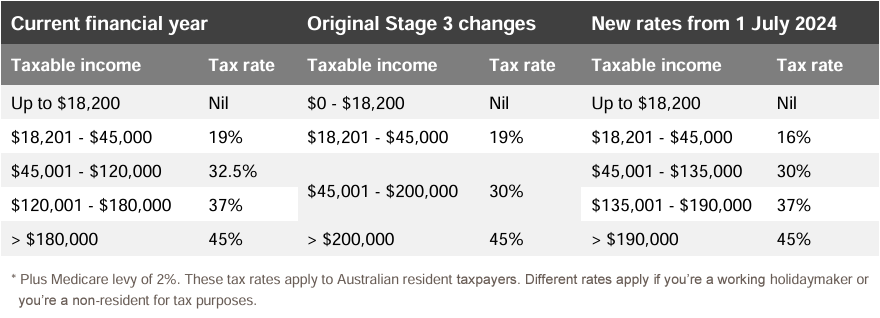

The ‘Stage 3 tax cuts’ were already law and due to come into effect on 1 July 2024. The recent amendments to the scheduled tax cuts change some of the personal income tax rates, as well as the income brackets that certain tax rates apply to. The tax-free threshold (which is the amount of income that you can earn before tax is payable), will remain at $18,200. Compared to the original tax cuts, the changes: ▪ reduce the 19% tax rate to 16% ▪ reinstate the 37% tax bracket (which was going to be removed from 1 July), but increase the income band to which this applies from $120,000 to $135,000, and ▪ decrease the threshold above which the 45% tax rate applies, from $200,000 to $190,000. The following table compares the tax rates for the current financial year with both the original Stage 3 tax cuts, and the new rates which are now law.

How will I receive the savings?

The changes to the tax rates will reduce the amount of tax that’s withheld from certain payments made to you. For example, employers and superannuation providers who pay you an income stream will make adjustments to the amount of tax withheld from these payments. This will result in incremental tax savings throughout the year. You don’t need to make changes to the way that you complete your tax return.

How much tax will I save?

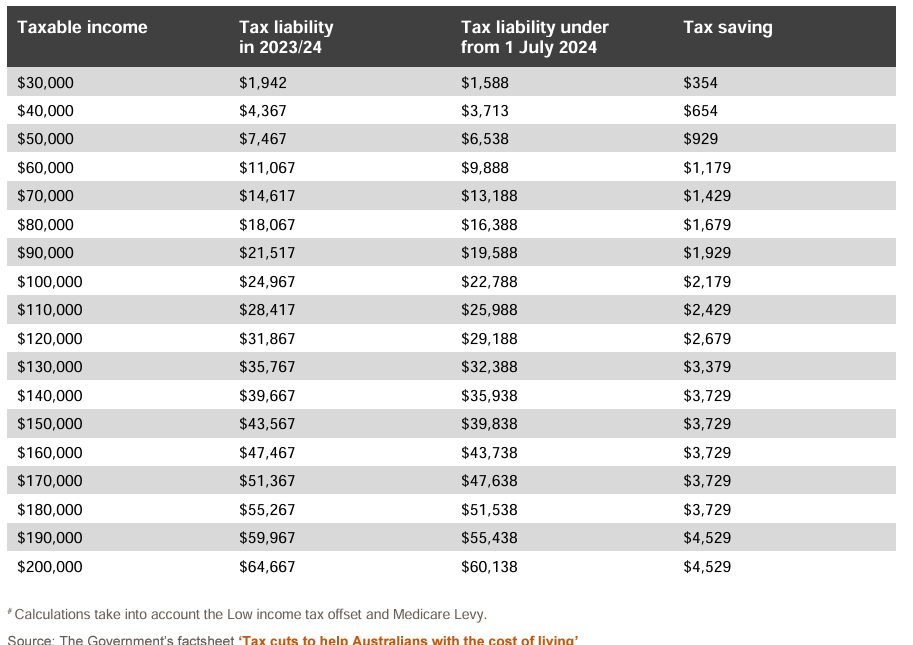

The amount of tax that may be saved at different levels of taxable income is summarised in the table below. You can also access a calculator on the Treasury website which estimates tax savings under the modified tax rates, compared to the tax payable in the current financial year.

What should I be thinking about as a result of the changes?

There’s no doubt that times are tough. With interest rate rises impacting loan repayments and other cost of living pressures, the tax savings may offer a great helping hand when it comes to meeting day to day expenses. However, there are strategies you may wish to think about and discuss with your financial planner, which could further boost the overall benefit of the savings.

Make your super work harder for you

One of the great things about superannuation is that there are so many ways to contribute, and even small contributions, such as those that attract a Government co-contribution, can make a big difference over time. Also, as your life and financial circumstances change, you can change your contributions strategy. That way, you can achieve what’s important to you and your family today, while still building your super nest egg.

There are even some ways you can contribute to super, which may provide additional tax benefits. For example, if you’re eligible, you can make voluntary after-tax contributions to super and claim a tax-deduction for these amounts. These are known as ‘personal deductible contributions’. Or you can make super contributions for your low-income spouse and benefit from aTo learn more about some of the different ways you could contribute, see our ‘Smart super strategies’ guide. It’s important to remember that once you contribute to super, you can’t access the funds until you meet a condition of release. This is usually when you retire, or meet other conditions which provide access to certain amounts, such as under the First Home Super Saver Scheme, or under financial hardship.

Consider the timing of your contributions

Were you thinking of making extra super contributions before the end of this financial year? You should consider the impact the newly legislated tax rates may have on the potential tax benefits. For example, if your marginal tax rate is still going to decline in 2024/25, you may gain a greater benefit by making a personal deductible contribution before 30 June this year. Conversely, if your marginal tax rate won’t change in 2024/25, the tax benefit from making a personal deductible contribution will be the same this financial year and next.

Thinking about selling assets?

Consider the timing Are you thinking of selling assets that would create a capital gain? If your marginal tax rate is going to be lower in 2024/25, you may pay less capital gains tax (CGT) by selling after 1 July this year.

But before you decide to defer any asset sale, it’s important to consider:

▪ market risk (the value of the asset could decline and offset or eliminate any tax benefit from selling next financial year), and

▪ holding costs, which for real property may include rates, insurance and interest payments.

Review the timing of your tax-deductible expenses including pre-paid expenses

Some expenses that you pay, including certain pre-paid expenses, are tax deductible. Pre-paying eligible expenses can be a helpful way to manage your tax. As a result of the change to the tax cuts from 1 July, you could consider whether the benefit of a tax deduction for eligible expenses is more valuable in the current financial year, or from 1 July 2024. This will depend on a couple of factors, including your assessable income, your marginal tax rate and the resulting value of the tax deduction.

Examples of deductible expenses that may be pre-paid include: ▪ premiums on an income protection policy held outside super ▪ interest on a fixed rate investment loan ▪ expenses for a rental property, and ▪ work related subscriptions. If you were planning to bring forward payment of eligible expenses (and therefore the associated deduction) to optimise your tax savings, you may need to review this strategy to work out the amount you save as a result of the changes.

For additional information on prepaid expenses, refer to the ATO website and confirm the deduction available with your registered tax agent.

Next steps

To find out more about the changes from 1 July and to understand more about which strategies could help to making your savings go even further, speak to your financial adviser. tax offset to reduce the tax you pay.

Important information and disclaimer