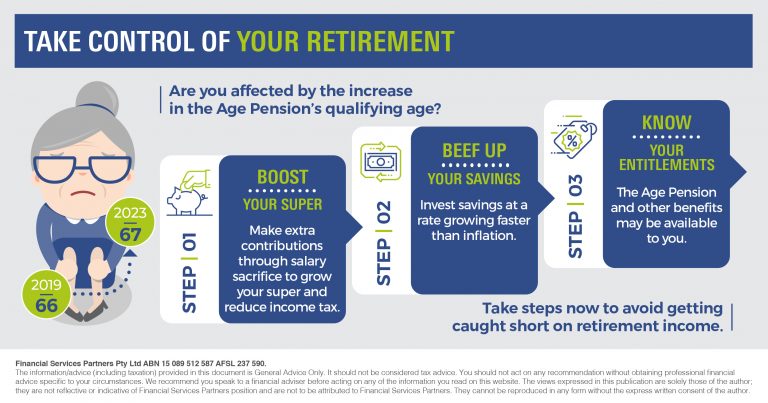

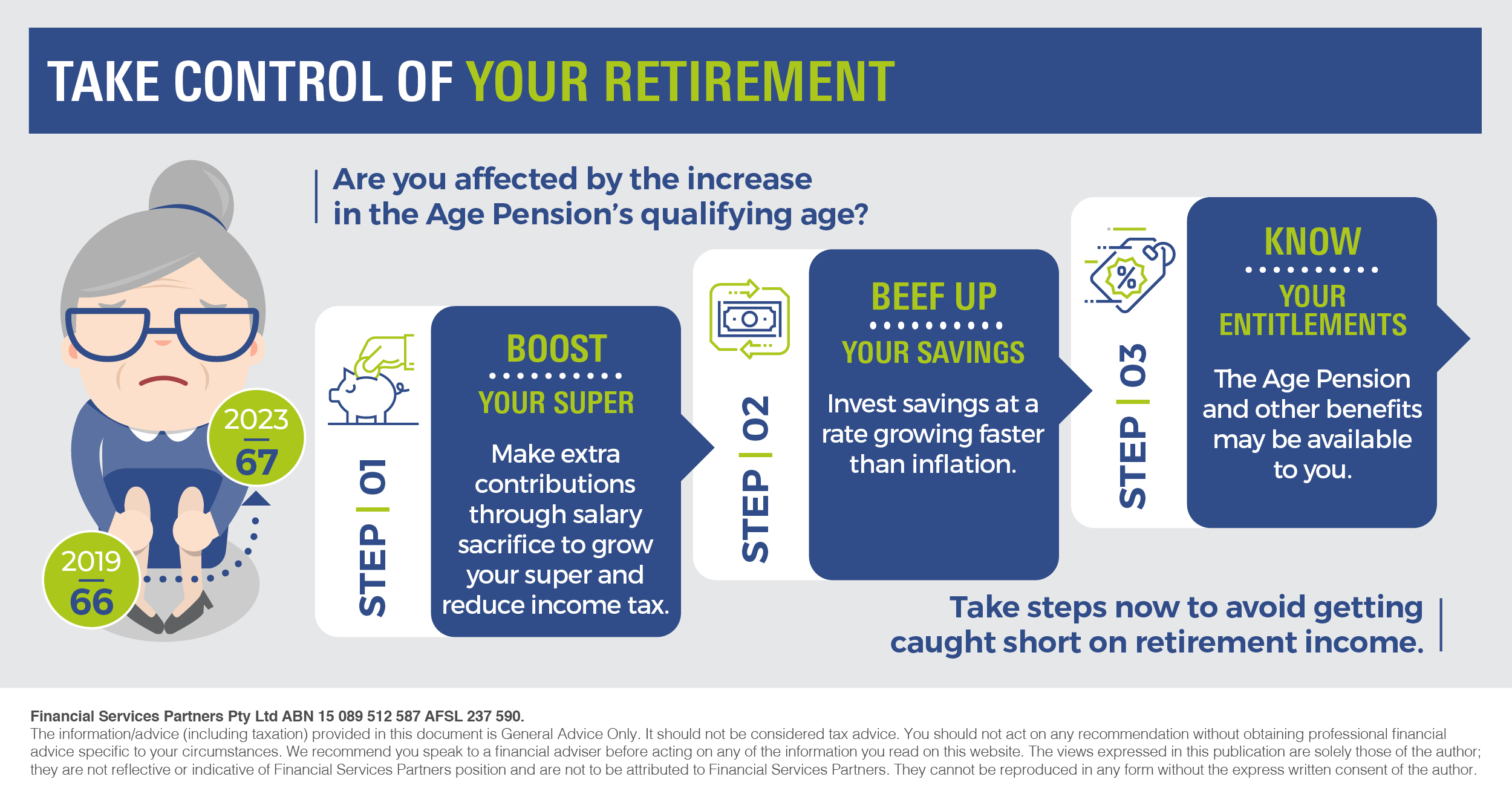

Take control of your retirement

Are you affected by the increase in the Age Pension’s qualifying age? Take steps now to avoid getting caught short on retirement income. The minimum age to qualify for the Age Pension has started going up. For those born on or after 1 July 1952, the qualifying age increases by six months every two years until it reaches 67 in July 2023. It rises to 66 in July this year.

So if you’re turning 45 this year and plan to retire when you reach 60, you will need to wait until you’re 67 before you can apply for the Age Pension. You’ll have to rely on your own savings and super in the interim, making it crucial to ensure you have enough money put away for later years. But the good news is that there’s still time to grow your retirement savings.

The minimum age to qualify for the Age Pension has started going up. For those born on or after 1 July 1952, the qualifying age increases by six months every two years until it reaches 67 in July 2023. It rises to 66 in July this year.

So if you’re turning 45 this year and plan to retire when you reach 60, you will need to wait until you’re 67 before you can apply for the Age Pension. You’ll have to rely on your own savings and super in the interim, making it crucial to ensure you have enough money put away for later years. But the good news is that there’s still time to grow your retirement savings.